From the “Livestock Monitor,” Livestock Marketing Information Center

DENVER – Based on producer surveys, USDA’s National Agricultural Statistics Service (NASS) significantly reduced the U.S. hay yield per acre for 2017, compared to earlier estimates, as reported in the Crop Production 2017 Summary released January 12th. That decline translated into a 1% drop in 2017’s national production estimate. At 131.5 million tons, U.S. total hay production was the smallest since 2012’s drought devastated crop, and was the third lowest since 1988.

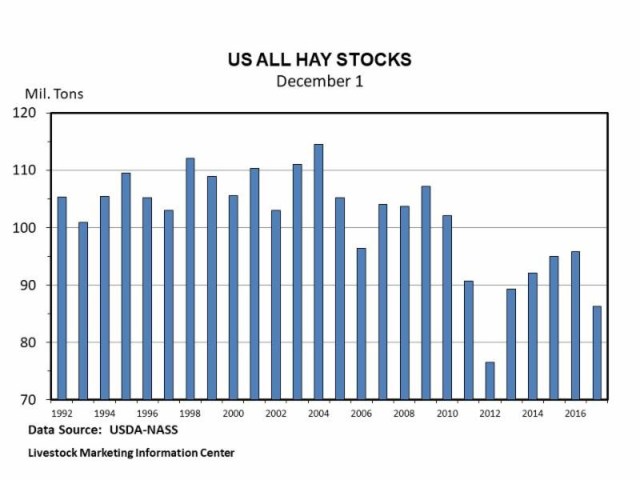

The NASS monthly Crop Production report (released January 12, 2018) contained their survey-based hay stocks as of December 1, 2017. At 86.2 million tons nationally, hay stocks were smaller than expected. U.S. stocks were 10% below a year earlier and the lowest since December 1, 2012, when severe drought limited hay production and increased late summer and fall usage. Note that the December 1, 2017, stock level was the second lowest since 1976. Year-over-year declines in stocks were associated with states impacted by drought, wildfires, and hay destroyed by hurricanes (flooding).

The arctic air mass that settled over much of the U.S., and in recent weeks even brought significant snow to southern states, likely causing much more hay to be fed to beef cattle than typical. Combining that with a cowherd that is larger than a year ago, resulted in the Livestock Marketing Information Center (LMIC) estimate of U.S. hay stocks to begin the new-crop year (as of May 1, 2018) as the smallest since 2013’s.

National alfalfa hay prices have posted year-over-year increases since the current crop-year began last May, and in November averaged $148.00 per ton, up $18.00 year-over-year (latest data available per NASS Agricultural Prices report). As of November, NASS reported the national “Other Hay” price was $118.00 per ton, down $2.00 from a year earlier. Hay price increases compared to 2017’s are likely this year. Helping keep a lid on hay prices are the values of other feedstuffs which are depressed (soybean meal, corn, etc.).

NASS reported new U.S. alfalfa seedings during 2017 were below 2016’s (down 3%). With normal growing conditions in 2018, U.S. hay production should increase compared to 2017’s. Still, total supply (May 1 stocks plus 2018 production) looks to remain historically tight, especially against a backdrop of more cattle.

That suggests higher national average hay prices well into 2018. Of course, hay is a regional crop, so not all states may see price gains. The LMIC projects that the national All Hay price in 2017/18 will average about $135.00 per ton, up $5.50 (about 4%) year-over-year. For the 2018/19 crop-marketing year, the preliminary LMIC forecast is for the national All Hay price averaging just over $150.00 per ton, the highest since 2014/15 ($172.00). Farmers that sell hay, especially high-quality types, may find that crop to be one of the few turning a profit in 2018.

From a livestock (cattle and sheep) market perspective, feedstuffs overall are likely to remain abundant in 2018. But, hay is a key ruminant animal feed and any impacts of drought in 2018 on pastures and/or hay production would be magnified by limited carry-over stocks, and could even cause some regional breeding herd/flock adjustments.

You must be logged in to post a comment.